What’s the best age to claim Social Security?

Key takeaways:

- Americans can start claiming Social Security as early as age 62, but the longer you wait, the more you’ll earn.

- If you wait until 70, your Social Security benefit can be up to 76 percent higher opens in a new window than if you start taking it at 62.

- It’s important to consider your health, financial needs and employment plans as you consider your benefit.

Many Americans consider Social Security a cornerstone of their retirement plans. But the rules around Social Security are complex, and choosing when to start claiming can dramatically impact how much money you end up receiving. Below is a breakdown of what your options are, and tips on how to make an informed decision.

What is Social Security?

Social Security is a U.S. federal program that provides Americans with retirement, disability and survivor benefits via payroll taxes. Both you and your employer contribute payroll taxes in each and every paycheck. Those funds go to current retirees, and your contributions earn you “credits” that make you eligible for benefits when you reach retirement age.

When can I start receiving Social Security?

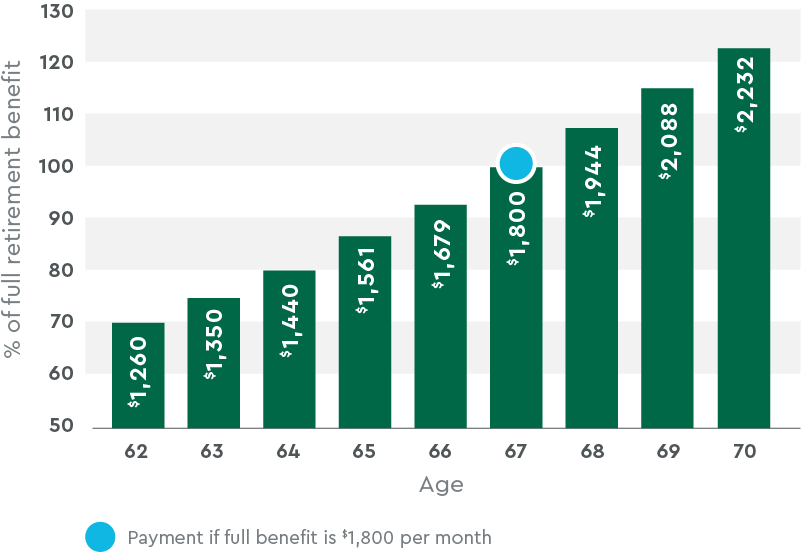

While you can start receiving your Social Security retirement benefits at 62, the amount you will receive grows each year you wait until you reach what the federal government calls “full retirement age. link opens in a new window” For those born after 1960, “full retirement age” is 67.

However, if you wait until age 70 to claim, you’ll receive the maximum monthly benefit. Here’s a breakdown of how claiming at various ages can impact the monthly benefit you’ll receive.

At what age should I claim Social Security?

It depends. While researchers at the National Bureau of Economic Research found that 70 is the ideal age opens in a new window for 90 percent of Americans to claim, many are choosing to collect sooner. In fact, the Financial Planning Association found that 64% of retirees opens in a new window who started claiming in 2022 chose to do so before their full retirement age.

When does it make sense to take Social Security early?

Those who claim Social Security before their official retirement age may choose to for a variety of reasons, including:

- Health status: Those with significant health concerns may prioritize accessing benefits sooner.

- You want or need to stop working: If you’re struggling to find work or ready to step away from the workforce, early benefits can ease the transition.

- Immediate income needs: If you need money now to cover basic expenses, early claiming provides an immediate lifeline.

- You’re maximizing family benefits: If you’re married, it’s important to weigh both of your ages and retirement benefits together, as it might make strategic sense for one spouse to claim earlier and the other later.

What are the downsides of taking Social Security early?

You may have been paying into Social Security your entire adult life, so it makes sense that you’re eager to start accessing it. But the earlier you claim it, the lower your monthly check will be — forever. And there are other impacts to consider:

- Reduced benefits over a lifetime: According to the UCLA Anderson Review, some Americans claiming at 62 instead of 70 may reduce their overall benefit by as much as 76% opens in a new window, depending on their income during working years and how long they live.

- Impact on spousal and survivor benefits: While Social Security is not an inheritable asset like an IRA or 401k, if you’re married, your spouse can either claim their own benefits or your benefits after you die, whichever one is greater. If there’s a large discrepancy between two spouses’ benefits or health, those factors should also be weighed.

- Earnings limitations if you keep working: If you claim benefits before your full retirement age but also continue working, Social Security may reduce your payments if you earn more than the annual limit ($22,320 in 2025). This can cut into your expected income as well.

- Short term gain vs. longer-term stability: Since benefits are designed to last a lifetime, locking in a lower amount early can make it harder to keep up with rising costs — especially healthcare expenses in your later years.

- For 50% of seniors, Social Security is at least 50% of their retirement income

- For 25% of seniors, it provides 90% or more of their retirement income

Before you decide, take a closer look at the numbers.

Deciding when to take Social Security is one of the biggest financial choices you’ll make for retirement. Run the numbers using a Social Security benefits calculator opens in a new window, and consider talking to a financial advisor. The longer you wait (up to age 70), the more you’ll get — but if you need it sooner, there are ways to make the most of early benefits.