How to understand your mortgage payment.

Whether you’re reviewing your loan estimate or examining your monthly mortgage statement for the first time, you might wonder, “What am I really paying for?” Mortgage payments consist of multiple elements, not just a single lump sum. Understanding each one could help you better manage finances as they relate to your new home.

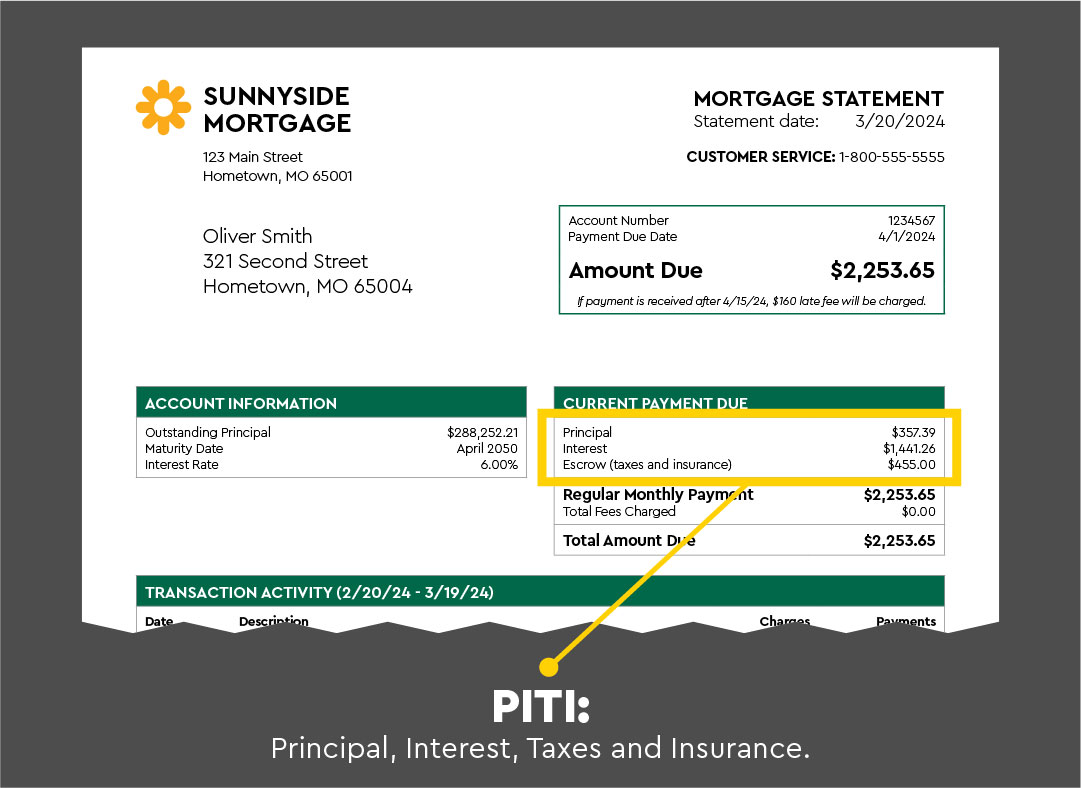

Mortgage payments typically consist of four main parts, often referred to as PITI: principal, interest, taxes and insurance. Let’s examine what each one means and how they might appear on your mortgage statement.

Principal.

The principal is the portion of your payment reducing your loan balance. This amount may increase slightly each month as your loan balance gets smaller.

Interest.

Interest is what you pay the lender to borrow money. This amount decreases slightly each month as more of the principal is paid off.

Escrow for taxes and insurance.

An escrow account is an account managed by your lender, and funded out of your monthly payment to make annual property tax and insurance payments for you. Other items like mortgage insurance and flood insurance may also get paid from this account. Lenders want to make sure your property is insured and that taxes are paid on time, reducing the risk that you default on the loan.

Did you know?

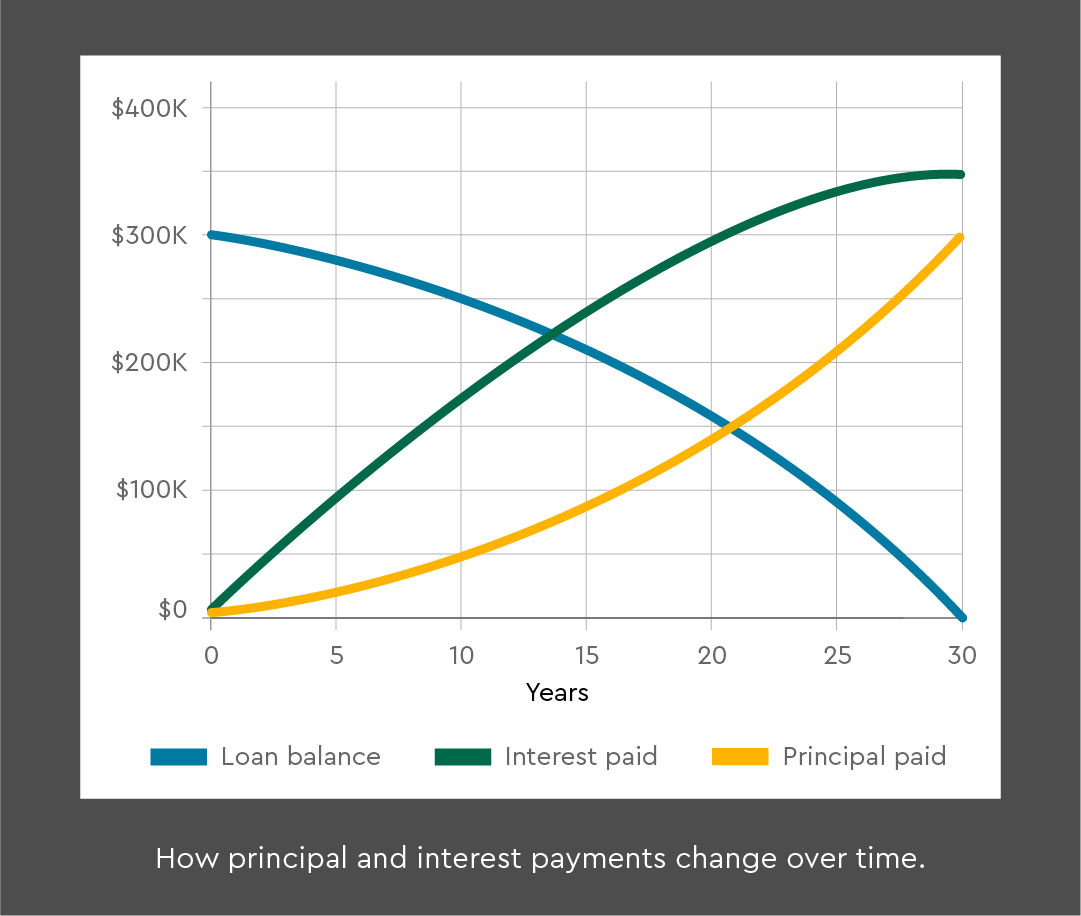

When you first take out a loan, a larger portion of your payment goes toward interest. As time goes on, more of your payment is applied to the principal. An amortization schedule provides a clear breakdown of how this occurs over the life of the loan. You can request a copy from your mortgage servicer.

Tip:

Make extra principal payments to pay off the loan faster than the amortization schedule. Speak with your mortgage servicer to confirm the money is applied to the principal loan balance, not interest.Taxes.

Property taxes fund local services like schools and road maintenance. They’re usually collected as part of the total mortgage payment and held in an escrow account by the mortgage servicer. This account is a secure holding place for the money before it’s released under specific conditions and at predetermined intervals.

Insurance.

Homeowners insurance protects your home from damage or loss. You likely selected an insurance policy before closing. Insurance premiums may also be collected by the mortgage servicer on your behalf. Similar to taxes, the money is held in an escrow account.

If you chose to pay taxes and homeowners insurance separately, then your statement would only reflect a required payment of principal and interest. However, if you put down less than 20% when buying your home, you may also see a charge for private mortgage insurance (PMI). This type of insurance protects the lender in case you do not repay the home loan as agreed.

PMI may be collected as part of the total mortgage payment or paid in another way, depending on lender options and borrower preferences.

Understanding escrow accounts.

Your mortgage statement should show escrow account activity. When taxes and home insurance premiums come due each year, the mortgage servicer is responsible for sending the money held in the escrow account to the applicable tax jurisdiction and your insurance company. The amount shown on the statement is the current balance.

How mortgage payments can change.

With a fixed-rate mortgage, your principal and interest payments stay the same, but your total payment can change if taxes or insurance costs fluctuate. If you have an adjustable-rate mortgage, your interest rate can change after a certain period, and your statement will reflect these changes.

Example mortgage statement breakdown.

For a $200,000 mortgage at 4% interest for 30 years:

- Principal and interest: $955

- Property taxes: $200

- Homeowners insurance: $67

- PMI: $75

Total monthly payment: $1,297

Did you know?

Missing a mortgage payment lowers your credit score and increases borrowing costs. Ensure payments arrive by the due date or before the end of the payment grace period. Most lenders give borrowers a 15-day grace period to allow for timing issues or minor oversights. Payments received 30 days or more after the due date are reported to credit bureaus. Mortgage lenders charge late fees opens in a new window as specified in the mortgage documents.

Understanding additional information on your statement.

Your mortgage statement contains valuable information beyond just payment amounts. Look for details about your outstanding principal balance, interest rate, payment due date, important messages or notices, and more from your mortgage servicer.

Each component of your payment serves a specific purpose, and regular reviews can help you spot issues and stay alert to upcoming adjustments and other important information related to the loan. Don’t hesitate to ask your mortgage servicer about any part of your statement you do not understand.

Staying informed about your mortgage through careful review of your statements is vital to managing your most valuable asset: your home.

Tips for managing mortgage payments:

- Review your statement carefully each month.

- Keep track of your escrow account balance.

- Consider making extra principal payments when possible.

- Contact your mortgage servicer if you see unexpected changes or have questions.

Disclosures:

To view or print a PDF file, Adobe® Reader® 9.5 or above is recommended. Download the latest version opens in a new window.